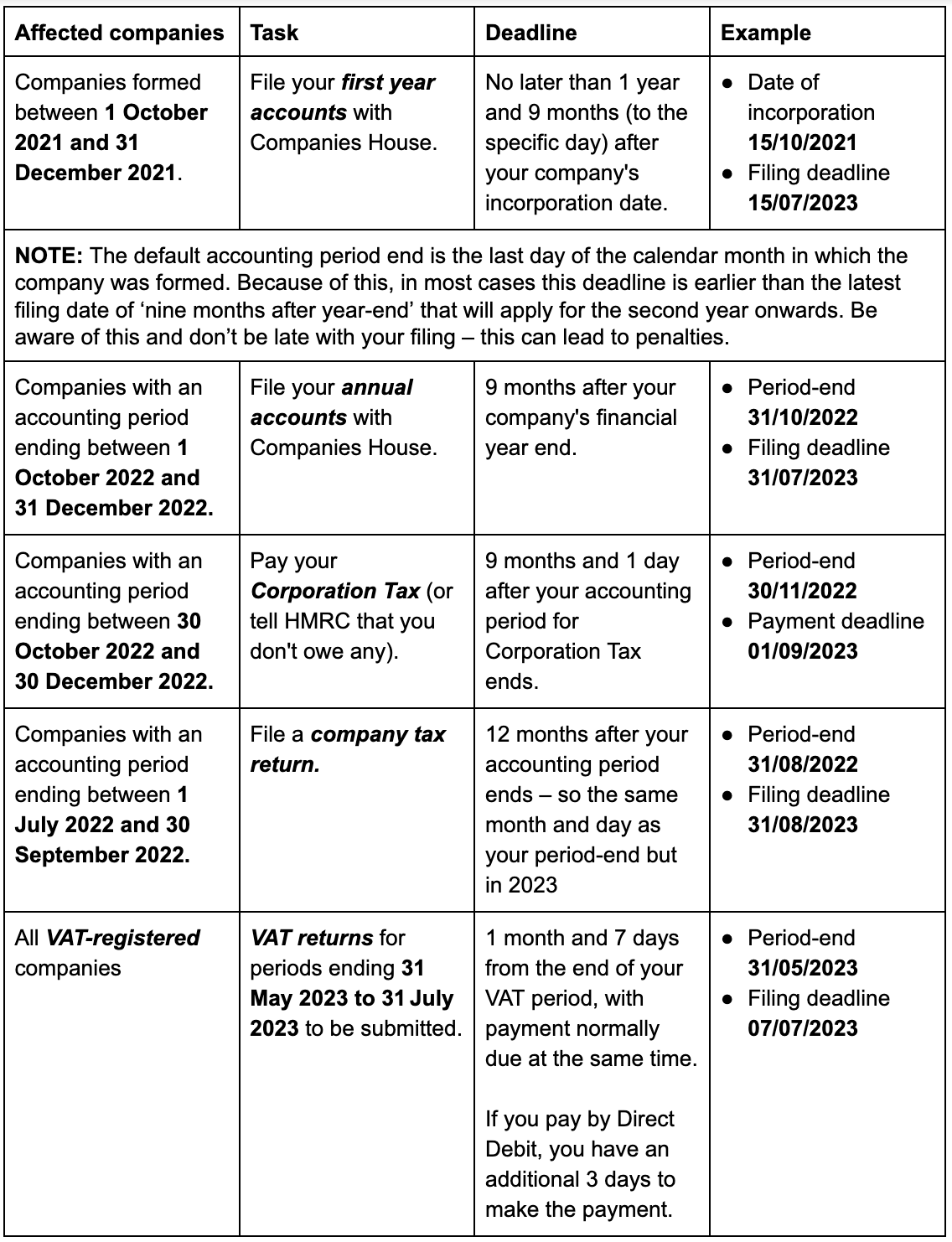

Your Q3 2023 deadlines for the diary

We’re always here to keep you up to date with the latest accounting, tax and compliance deadlines. Here are the forthcoming deadlines and cut-off points for Q3 of 2023 to add to your diary.

NOTE: If your company’s accounting period is longer than 12 months, the first tax payment deadline is normally 21 months and 1 day after your accounting period started, and the second one is 9 months and 1 day after your accounting period ends.

For example, a company with an accounting period running from 01/09/2021 to 31/12/2022 will pay the first tranche of corporation tax by 01/06/2023 and the balance by 01/10/2023.

If your profits are more than £1.5 million, then tax is payable quarterly with two payments before the end of your accounting period and two after. The first payment is normally six months and 13 days after the start of the period, with the others three-monthly from that point.

Some general deadlines to plan for:

- Employment related securities (ERS) schemes need to be registered (for the previous tax year): 6 July 2023

- ERS Annual Return (for previous tax year) must be submitted: 6 July 2023

- Enterprise Management Incentives (EMI) schemes ‘notice of options granted’ to be submitted: within 92 days of grant.

- Submit your P11D, P11D(b) and P9D returns (for 2022/23 tax year): 6 July 2023

- Pay Class 1A National Insurance contributions to HMRC (for 2022/23 tax year): 19 July 2023

- Make your second payment on account for 2022/23 personal tax: 31 July 2023

- Make Capital Gains Tax payment for gains on residential property: 60 days after completion

- PAYE and National Insurance payments due: 19th calendar day of the month after end of month or quarter as applicable (22nd for electronic payments)

Talk to us about hitting your deadlines

If we’re looking after your payroll and tax returns, we’ll be monitoring these dates and deadlines automatically – but don’t forget that you remain legally responsible for meeting all deadlines.

Keep an eye on all the upcoming deadlines and check the upcoming dates for all relevant activities. Pay particular attention to those where we don't carry out the task for you. Missing a compliance deadline can result in fines and penalties, so it’s good practice to keep everything well-organised and on time.

Get in touch to discuss your deadlines.